Most people are told to avoid debt completely. But the truth is more nuanced — not all debt is harmful. When used wisely, debt can help you build wealth, invest in your future, and create financial opportunities. However, when used poorly, debt can trap you in a cycle that becomes difficult to escape.

Understanding the difference between good debt vs bad debt is one of the most important financial skills you can develop. Once you learn how debt works and how to avoid common debt traps, you can make smarter financial decisions that support long-term stability.

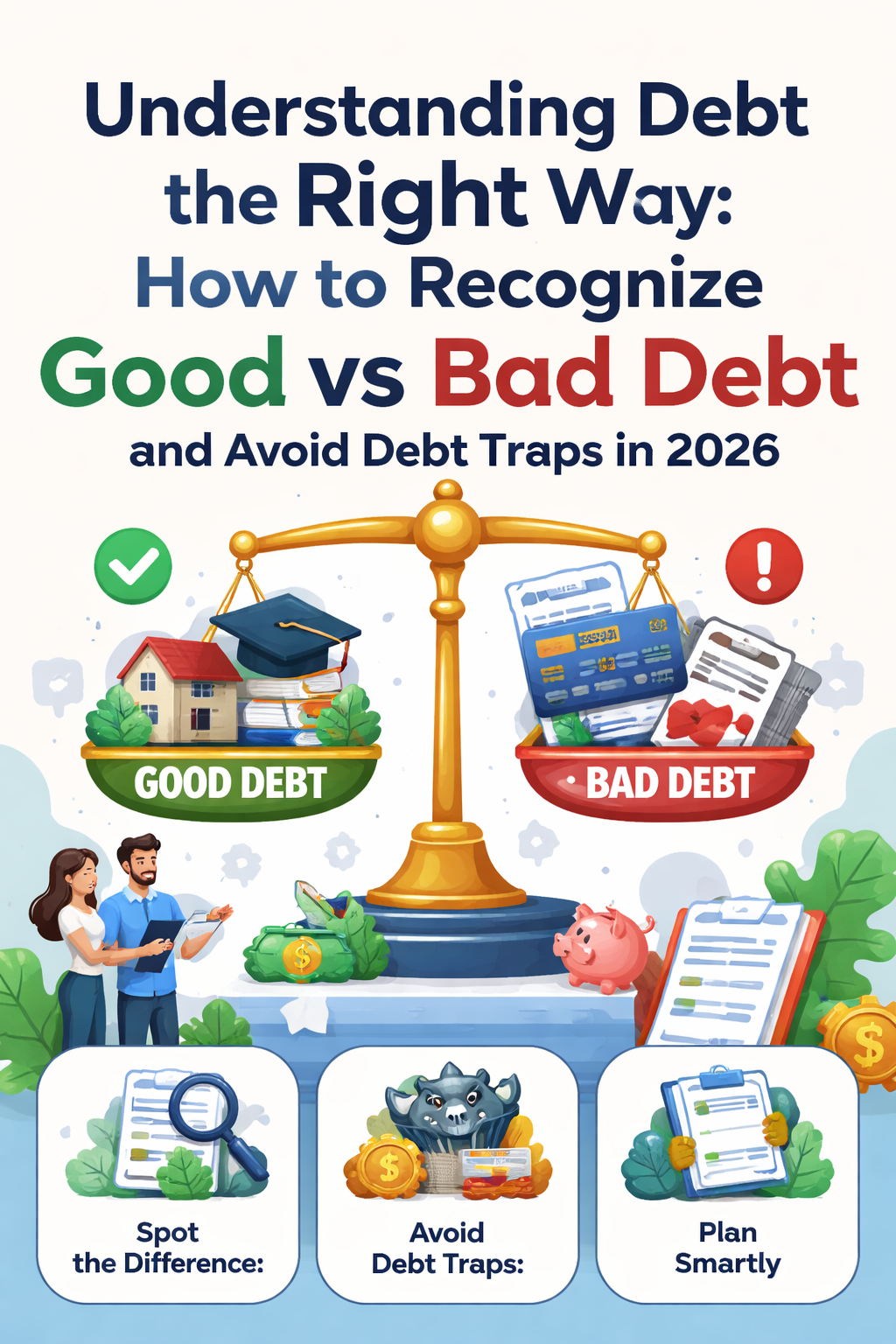

Direct Answer: What Is Good Debt vs Bad Debt?

Good debt is borrowing money for something that has the potential to improve your financial situation or increase your long-term value, such as education, a home, or starting a business. Bad debt, on the other hand, is borrowing for things that lose value quickly or create ongoing financial pressure, such as high-interest credit cards, payday loans, or unnecessary purchases.

The key difference is simple: good debt helps build your future, while bad debt makes your financial life harder.

What Is Debt and Why It Matters

Debt is money you borrow that must be repaid over time, usually with interest. While borrowing can provide access to opportunities, interest payments mean you often repay more than you originally borrowed.

This is why understanding debt matters. Used wisely, debt can help you:

- Build credit history

- Invest in long-term assets

- Improve earning potential

- Handle emergencies responsibly

Used poorly, debt can:

- Reduce your monthly cash flow

- Increase financial stress

- Delay savings goals

- Make it harder to build wealth

Many people fall into financial difficulty not because they borrow money, but because they borrow without understanding the long-term impact. This is why learning the right way to use debt is essential.

What Is Good Debt?

Good debt is typically associated with borrowing that has the potential to improve your financial future. It often comes with lower interest rates and structured repayment plans.

Examples of Good Debt

Student Loans

Education can increase your earning potential over time. Borrowing for education may be considered good debt when the program improves your career prospects and future income.

However, this only applies when borrowing is reasonable and aligned with realistic income expectations. Taking on excessive student loans without a clear plan can still create financial challenges.

Mortgage Loans

Buying a home is often considered good debt because real estate typically appreciates over time. Instead of paying rent, your payments go toward ownership.

Additionally, homeownership can provide long-term financial stability and potential equity growth.

Business Loans

Borrowing money to start or expand a business can also be considered good debt, especially when the business has strong growth potential.

Many successful entrepreneurs use debt strategically to scale their businesses, invest in equipment, or expand operations.

Strategic Personal Loans

Sometimes, personal loans used to consolidate high-interest debt into a lower-interest option may also be considered good debt.

For example, consolidating multiple credit cards into one lower-interest payment can simplify finances and reduce interest costs.

This concept is closely related to How to Stop Living Paycheck to Paycheck, where managing obligations effectively improves overall financial stability.

What Is Bad Debt?

Bad debt usually involves borrowing for items that lose value quickly or create ongoing financial strain. These types of debt often carry higher interest rates and fewer long-term benefits.

Examples of Bad Debt

High-Interest Credit Card Debt

Credit cards can be useful when managed responsibly. However, carrying balances with high interest rates can quickly lead to long-term debt.

Minimum payments may seem manageable, but they extend repayment timelines and increase total interest paid.

This is why understanding Budgeting Mistakes Beginners Must Avoid in 2026 is important, since poor budgeting often leads to excessive credit card reliance.

Payday Loans

Payday loans often come with extremely high interest rates and short repayment terms. These loans can quickly turn into a debt cycle, especially if borrowers need to take new loans to repay old ones.

This is one of the most common debt traps people experience.

Buy Now, Pay Later Overuse

Buy now, pay later services can be helpful in moderation. However, using multiple payment plans simultaneously can create confusion and lead to missed payments.

This can also negatively affect your credit score and overall financial health.

Unnecessary Consumer Debt

Borrowing money for items that quickly lose value — such as luxury purchases, gadgets, or impulse buys — is often considered bad debt.

These purchases do not improve financial stability but still require repayment with interest.

How Debt Traps Happen

Debt traps often develop gradually rather than suddenly. Small borrowing decisions can accumulate over time and become difficult to manage.

Common causes of debt traps include:

- Relying on credit cards for everyday expenses

- Not having an emergency fund

- Taking multiple loans simultaneously

- Ignoring interest rates

- Making only minimum payments

Without a plan, these habits can create a cycle where most of your income goes toward debt payments.

This is why building an emergency cushion, as discussed in How to Build an Emergency Fund From Scratch, can help reduce reliance on debt during unexpected situations.

How to Avoid Debt Traps

Avoiding debt traps requires intentional planning and disciplined financial habits.

1. Borrow Only When Necessary

Before taking on debt, ask yourself:

- Do I really need this?

- Will this improve my financial situation?

- Can I afford the monthly payments?

If the answer is no, it may be best to delay borrowing.

2. Understand Interest Rates

Interest rates determine how much extra you pay over time. Even a small difference in rates can significantly increase total repayment.

Always compare options before borrowing.

3. Build an Emergency Fund

Emergency savings reduce the need for borrowing during unexpected situations like job loss, medical expenses, or urgent repairs.

Even small savings can prevent high-interest debt.

4. Avoid Minimum Payments

Minimum payments extend repayment timelines and increase interest costs. Paying more than the minimum reduces debt faster.

5. Track Your Debt

List all your debts, including:

- Balance

- Interest rate

- Minimum payment

- Due date

Tracking helps you stay organized and create a repayment strategy.

Tips for Using Debt Wisely

Debt is not always negative. When used strategically, it can support financial growth.

Here are smart ways to use debt:

- Borrow for income-producing opportunities

- Keep debt manageable

- Maintain a strong credit score

- Pay on time consistently

- Avoid borrowing for lifestyle upgrades

These strategies align with long-term financial planning and responsible money management.

Signs Your Debt Is Becoming a Problem

Watch for these warning signs:

- You rely on credit cards for essentials

- You struggle to make minimum payments

- You borrow to repay other debts

- Your debt keeps increasing

- You feel constant financial stress

If you notice these signs, it may be time to reassess your financial strategy and focus on repayment.

Building a Healthy Relationship With Debt

The goal is not to avoid debt completely but to use it wisely. Responsible borrowing can help you:

- Build credit

- Invest in opportunities

- Improve financial flexibility

- Achieve long-term goals

However, discipline and planning are essential.

When you understand debt properly, you gain control over your financial future instead of allowing debt to control you.

This ties closely into other areas that often get overlooked at the beginner stage. Read: Retirement Planning by Age: What to Do in Your 30s, 40s, and 50s to Build a Secure Future

Final Thoughts

Understanding debt the right way is one of the most important steps toward financial stability. Good debt can create opportunities, while bad debt can create obstacles.

By learning to recognize the difference and avoiding common debt traps, you position yourself for smarter financial decisions and long-term growth.

Start by borrowing intentionally, managing repayments responsibly, and building savings to reduce reliance on debt.

Over time, these habits can help you build a stronger financial foundation and move closer to your long-term financial goals.

Frequently Asked Questions

Good debt is used for investments that increase long-term value, such as education, a home, or a business. Bad debt is borrowing for items that lose value quickly or create financial stress, like high-interest credit cards, payday loans, or luxury items.

Yes. When used wisely, debt can help you build credit, invest in opportunities, and achieve financial goals. Strategic borrowing, like a mortgage or student loan, can improve your long-term financial position.

Common debt traps include relying on high-interest credit cards, payday loans, multiple buy now-pay later plans, and borrowing for unnecessary consumer purchases. These can create cycles of ongoing debt and financial stress.

Avoid bad debt by borrowing only when necessary, understanding interest rates, building an emergency fund, paying more than the minimum on loans, and tracking all your debts carefully.

Warning signs include relying on credit cards for essentials, struggling to make minimum payments, borrowing to pay off other debts, increasing debt levels, and experiencing constant financial stress. Recognizing these early allows for corrective action.